This blog was first published in Brookings Future Development Blog. The authors, Ipchita Bharali and Indermit Gill have authored a policy brief and a report “Enhancing domestic revenues: constraints and opportunities” available for download here.

Developing countries should expect foreign aid to fall during the transition from low to middle income, and end soon after. In low-income countries, the share of foreign aid is about 2.5 percent of GDP. This drops to 0.8 percent in lower-middle-income economies; by upper-middle-income levels, it is a negligible 0.2 percent.

For both givers and receivers of foreign assistance, one of the main concerns is that foreign aid weakens the incentives to build domestic revenue administration capacity and make sensible tax policy choices. The stakes can be high. Even a pre-announced and gradual reduction of foreign aid might jeopardize hard-won gains in health, education and public security, because governments may not be able to muster domestic funds for what donors were supporting. But how can a donor decide whether the government is making an honest effort to reduce its dependence on outside help? A new report by Duke University’s Center for Policy Impact in Global Health might help in doing just that.

Distinguishing capability from conscientiousness

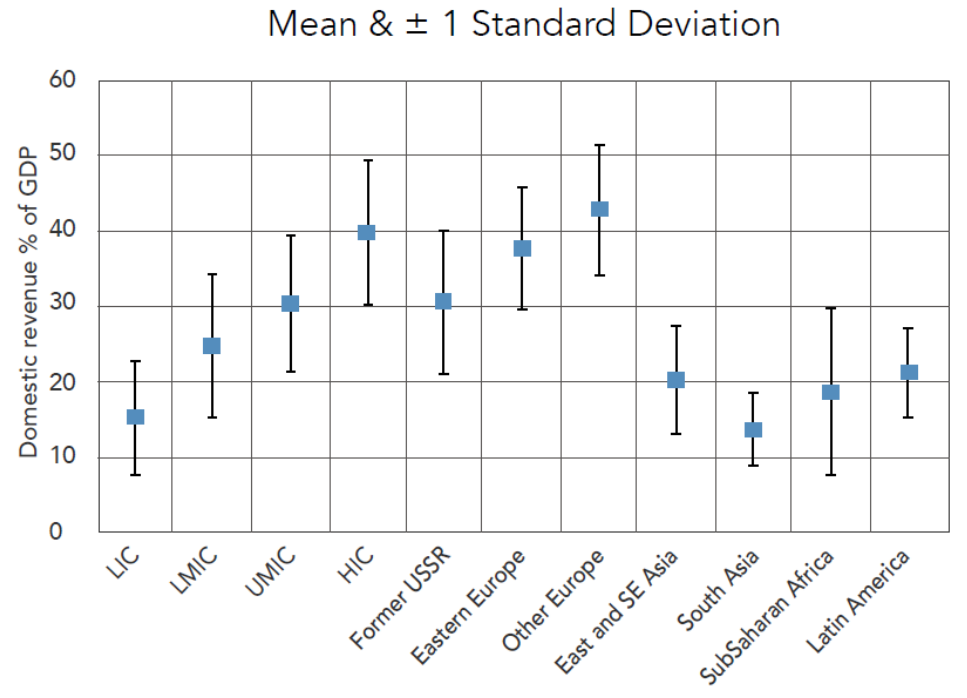

As countries develop, their economic structures change. Relatedly, the size of government increases. One reason is that as the economy becomes more monetized, more activities can be taxed. Typically, the share of domestic revenues is 15 percent of GDP in low-income economies, 25 percent in lower-middle-income countries, 30 percent in upper-middle-income countries, and 40 percent in advanced economies. This is to be expected. Less easily justifiable is the variation in domestic revenue mobilization within these groups. In low-income countries, for example, governments may collect as little as 7.5 percent of GDP in revenues and as much as 22.5 percent. This ratio ranges between 15 and 35 percent among lower-middle-income economies, and between 20 and 40 percent among upper-middle-income countries (Chart 1).

Chart 1: Share of Domestic Revenues in GDP

Source: Glenday et. al. (2018)

Clearly, a country’s income is not all that matters for how much its government collects as taxes. Governments can do a lot, or not much, to bring in revenues. The problem is how to figure out whether they are doing all that they could. This involves answering three questions:

- How much domestic revenues should a country be reasonably mobilizing—that is, what is its tax capacity?

- What are the reasons a government is not raising the tax and nontax revenues it needs—that is, what is the main reason for the gap between capacity and performance?

- What are the implications for governments and for donors—that is, how should aid relationships change as developing countries approach income transitions?

Estimating revenue capacity

For a developed country, the size of government, approximated by the ratio of public expenditures to GDP, can be a matter of societal choice. Differences in South Korean and French expectations of their respective states could explain the 20 percentage-point difference in government size. But for a developing economy, this choice is constrained less by societal preferences and more by its economic structure, administrative capacity, and policy choices.

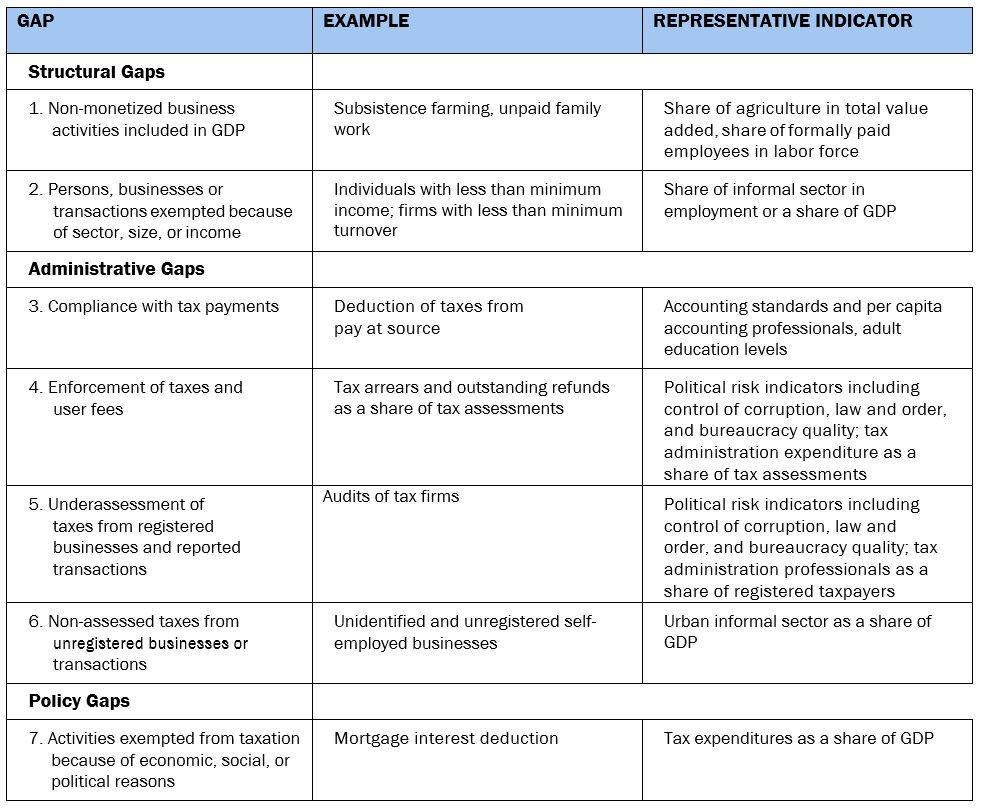

Tax capacity can reasonably be gauged using measures of these factors, summarized in Chart 2. The tax capacity calculated using these indicators is then compared with the actual revenue effort. The difference is an obvious measure of the “revenue gap.”

Chart 2: Measures of the gaps between revenue capacity and effort

Source: Adapted from Glenday et. al. (2018).

With some more work, we can estimate how much of this gap is due to the difference in economic characteristics of a country relative to its peers, how much is because of lower-than-average administrative capacity, and how much can be attributed to tax policy differences with its peers. The decomposition into characteristics, capacities, and choices is useful for deciding what to expect. While all three can be altered by government policy, we should expect economic characteristics to change over long periods, state capacity to be increased somewhat more quickly, and public policy choices to be altered even quicker.

Identifying underperformance

The next step is to obtain this information on every country’s characteristics, capacities, and choices—low, middle, and high income—and identify each economy’s revenue capacity. The data to calculate these gaps are not always readily available, especially for developing economies, and generally have to be cobbled together from multiple sources. Often, less than ideal substitutes have to be used. This problem is especially acute for administrative capacity and policy choices. But, if carefully done, the estimates provide information that can be used to inform the dialogue between donors and countries in the middle of an income transition.

The findings are generally reassuring (Chart 3). There is a big step-up in both tax and nontax revenues as countries develop from low- to middle-income levels, and continued increases during middle-income. Disconcertingly though, improvements in tax performance seem to slow down after countries reach lower-middle-income levels.

Chart 3: Revenue increments with income transitions

Source: Glenday et. al. (2018).

Besides, aggregate statistics hide a lot of variation within each group. To get a complete picture, the first step consists of analysis to account for the factors that influence the amount of taxes or revenues a country should reasonably collect: societal preferences, natural resources, economic structure, administrative capacity, and tax policies. The analysis yields useful findings.

- Among low-income economies, economic structure matters the most. Foreign aid appears to increase the tax to GDP ratio. Administrative capacity does not seem to matter, but the tax rate does. Revenue performance is lowest in low-income East Asia.

- Among lower-middle-income economies, the availability of foreign assistance may reduce the ratio of domestic revenues to GDP. Administrative capacity does not seem to matter, but the tax rate does. Holding other things constant, revenue collections are higher in Europe and Central Asia, and lowest in South Asia.

- In upper-middle-income economies, the determinants are essentially the same as for lower-middle-income countries. The main differences are that higher global non-energy commodity prices and larger shares of mining in GDP seem to increase revenue performance somewhat, and Latin American and East Asian economies underperform.

- In high-income economies, what really seems to matter for domestic revenues is the composite tax rate. Economic structure is less important, and societal choices are reflected largely in personal and corporate income tax rates and sales or value-added tax rates.

The final step entails determining the tax and domestic revenue capacities given the economic characteristics, administrative efficiency levels, and tax policy choices that a country in its income class is expected to have. This is done using a simple regression analysis. The tax and domestic revenue capacity is then compared to the actual taxes or revenues collected by the country in the year. Countries can then be classified by effort. A ratio of actual tax/revenues to tax/ revenue capacity of one implies that a country is performing at potential (Chart 4).

Chart 4: Countries classified by revenue effort

Source: Glenday et. al. (2018): Table 7.9.

Upper-middle-income countries have upped their effort over the last two decades, but the performance of low- and lower-middle-income countries appears to be declining. When combined with the findings discussed above, these results are especially of concern for lower-middle-income countries.

Finding a fix

The findings of the report provide useful pointers for improving public financial management, mobilizing domestic resources, and reducing aid dependence. Three seem to stand out.

Better measures of the quality of tax administration. The study utilized the World Bank Worldwide Governance Indicators and political risk indicators from the International Country Risk Guide Researchers’ Dataset. More reliable measures would have been those estimated using the assessment of tax administration using the International Monetary Fund’s Tax Administration Diagnostic Assessment Tool (TADAT). But these assessments were available for only 12 countries until July 2018. The first step towards greater domestic revenue mobilization should be an expansion of the coverage of TADAT assessments.

Much more attention to tax expenditures. Tax expenditures range between 4 and 8 percent of GDP in developing economies, but they are often measured badly and reported irregularly. Even where they are regularly reported, they are generally estimated only for the central government. Tax expenditures are the least transparent parts of government spending, prone to misdirection and capture by privileged segments, or outright corruption. A tight grip on tax expenditures is a big part of good domestic resource mobilization.

A special focus on lower-middle-income economies. It is hard to miss the relatively small increase in taxes and contributions in the transition from lower to upper-middle-income levels. While the average per capita GDP of the typical upper-middle-income economy is nearly triple that of the average lower-middle-income country, the average ratio of taxes and contributions to GDP increases by just 4 percentage points (Chart 3). Disturbingly, foreign aid weakens revenue mobilization in lower-middle-income economies (but not in low-income countries). In countries such as Egypt, Nigeria, Pakistan, and Guatemala where revenue performance is weak, donors should worry that they may be discouraging domestic resource mobilization efforts.

About the Authors:

Indermit Gill is the Director of the Duke Center for International Development.

Ipchita Bharali (@IpchitaBharali ![]() ) is a Policy Associate at the Center for Policy Impact in Global Health, Duke Global Health Institute.

) is a Policy Associate at the Center for Policy Impact in Global Health, Duke Global Health Institute.